How to Build a Strong Credit Score by Swiping Your Credit Card

Table of Contents

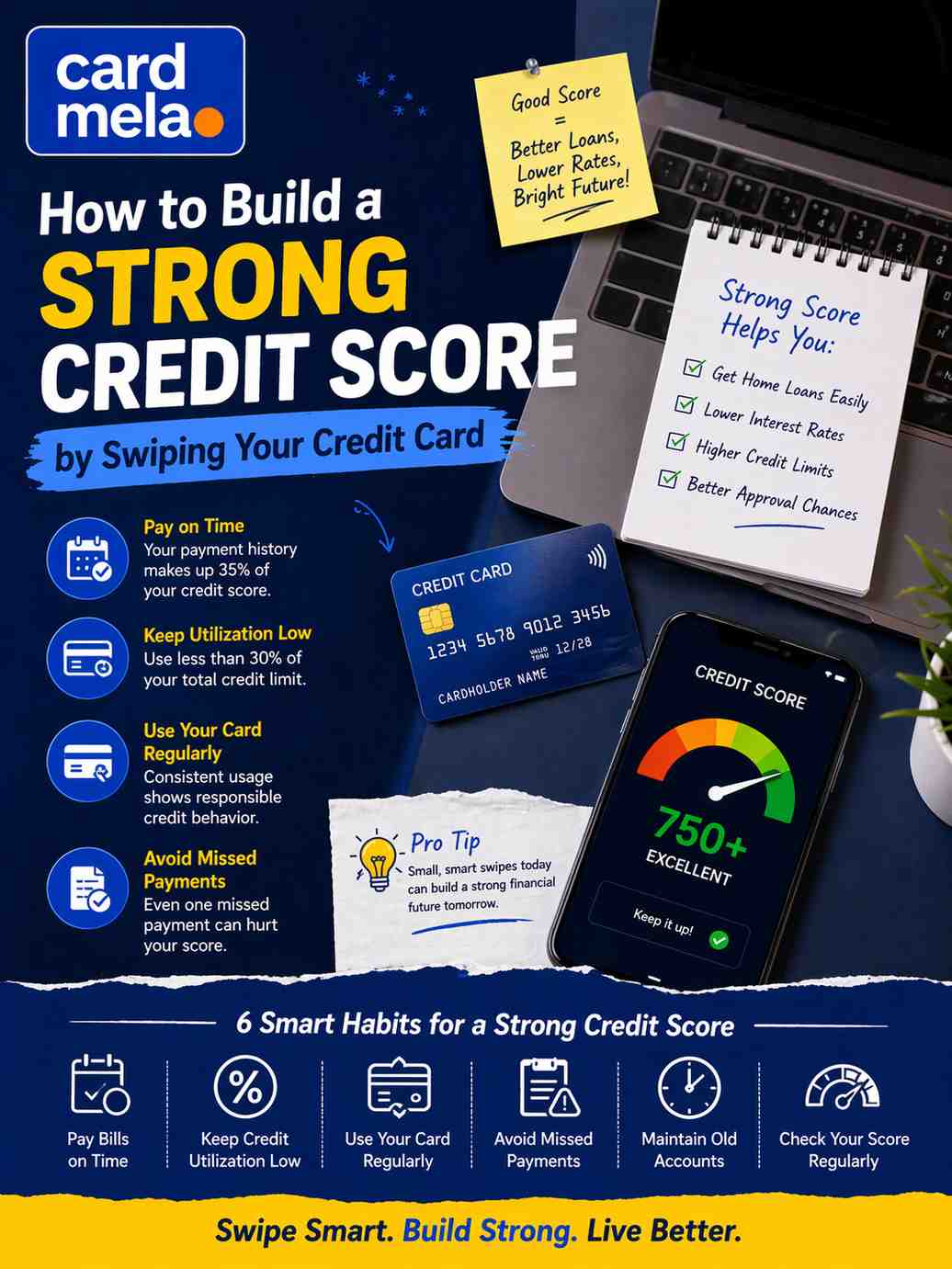

How to Build a Strong Credit Score by Swiping Your Credit Card (2026 Guide)

Introduction

In today’s digital financial ecosystem, building a strong credit score is no longer optional—it is a necessity. Whether you plan to apply for a home loan, car loan, or even a premium credit card, your credit score determines your financial credibility. In India, institutions like TransUnion CIBIL track your credit behavior and assign a score that reflects your repayment discipline and credit usage patterns.

One of the most powerful and accessible tools for improving this score is a credit card. Every swipe you make contributes to your credit profile, making credit cards a daily opportunity to build financial strength. Banks such as HDFC Bank, ICICI Bank, Axis Bank, and State Bank of India offer a wide range of cards designed for beginners as well as experienced users.

However, simply owning a credit card is not enough. The real impact comes from how you use it. Strategic swiping, disciplined repayment, and smart credit utilization can gradually transform your credit profile. This guide will help you understand how to use credit cards effectively to build a strong credit score and unlock better financial opportunities.

Explanation: How Credit Card Usage Impacts Credit Score

Your credit score is influenced by multiple factors, and credit card usage directly affects several of them. The most important factor is payment history. Timely payment of credit card bills demonstrates financial responsibility and contributes positively to your score.

Another crucial factor is credit utilization ratio, which refers to the percentage of your total credit limit that you use. Keeping utilization low (ideally below 30%) signals that you are not overly dependent on credit, which improves your score.

The length of your credit history also plays a role. The longer you maintain an active credit card account with good repayment behavior, the stronger your credit profile becomes. Additionally, having a mix of credit types, including credit cards, can further enhance your score.

Each swipe you make, therefore, is not just a transaction but a data point that contributes to your overall creditworthiness.

Benefits of Building a Strong Credit Score

A strong credit score provides long-term financial advantages that go beyond immediate savings. One of the most significant benefits is easier access to loans. Banks are more likely to approve loan applications for individuals with high credit scores, often offering better interest rates and higher loan amounts.

Another advantage is financial flexibility. With a strong credit profile, users can access premium credit cards, higher limits, and exclusive financial products. This enhances both spending power and financial convenience.

A good credit score also reduces the cost of borrowing. Lower interest rates on loans can save a substantial amount of money over time, making large financial goals such as buying a home or car more affordable.

Additionally, a strong credit score builds trust with financial institutions. It reflects disciplined financial behavior, which can open doors to better opportunities and faster approvals in the future.

Uses of Credit Cards for Credit Score Improvement

Credit cards can be used strategically to build and maintain a strong credit score. One of the most effective uses is making regular, small transactions and repaying them on time. This creates a consistent record of responsible credit usage.

Another practical use is managing recurring expenses. Payments for subscriptions, utilities, and online purchases on platforms like Amazon and Flipkart can be routed through credit cards to maintain regular activity.

Users can also use credit cards to maintain a low utilization ratio by spreading expenses across multiple cards. This ensures that no single card is heavily utilized, which helps maintain a healthy credit profile.

Over time, these practices build a strong credit history that positively impacts the credit score.

Best NEW Credit Cards for Building Credit Score

IDFC FIRST Classic Credit Card

- Ideal for beginners

👉 Apply Now on CardMela

HDFC Bank Freedom Credit Card

- Easy approval + consistent usage

👉 Apply Now on CardMela

Axis Bank Insta Easy Credit Card

- Perfect for low credit score users

👉 Apply Now on CardMela

ICICI Bank Platinum Chip Credit Card

- Simple and effective usage

👉 Apply Now on CardMela

SBI Unnati Credit Card

- Good for first-time users

👉 Apply Now on CardMela

Flipkart Axis Bank Credit Card

- Regular usage improves credit history

- High approval rate

Amazon Pay ICICI Credit Card

- Ideal for frequent online users

👉 Apply Now on CardMela

AU Bank LIT Credit Card

- Flexible usage improves utilization management

👉 Apply Now on CardMela

RBL Bank Platinum Maxima Credit Card

- Good for consistent spending

👉 Apply Now on CardMela

Yes Bank Prosperity Cashback Credit Card

- Helps maintain active usage

👉 Apply Now on CardMela

Credit Score Factors Breakdown

| Factor | Weightage | Impact |

|---|---|---|

| Payment History | 35% | Very High |

| Credit Utilization | 30% | High |

| Credit History Length | 15% | Medium |

| Credit Mix | 10% | Medium |

| New Credit | 10% | Low |

Credit Score Factors Table

| Factor | Weightage (%) | Impact on Score | Tip |

|---|---|---|---|

| Payment History | 35% | 🔴 Very High | Hamesha on-time payment karo |

| Credit Utilization | 30% | 🔴 High | 30% se kam usage rakho |

| Credit History Length | 15% | 🟡 Medium | Old cards close mat karo |

| Credit Mix | 10% | 🟢 Low | Loans + cards mix rakho |

| New Credit Inquiries | 10% | 🟡 Medium | Bar-bar apply mat karo |

Smart vs Poor Credit Card Usage

| Behavior | Impact on Score |

|---|---|

| Timely Payments | Positive |

| High Utilization | Negative |

| Missed Payments | Very Negative |

| Long Usage History | Positive |

Tips

Building a strong credit score through credit cards is not about how much you spend, but how responsibly you manage your spending. One of the most important tips is to maintain consistency in usage. Instead of making occasional large transactions, users should focus on regular, small payments such as utility bills, subscriptions, and daily expenses. This creates a steady record of activity that positively impacts the credit profile.

Another critical strategy is to keep credit utilization under control. Using more than 30% of your total credit limit can signal financial stress to lenders, even if you pay your bills on time. Distributing expenses across multiple cards or requesting a limit increase can help maintain a healthy utilization ratio.

Timely repayment is the most powerful factor in building a strong credit score. Missing even a single payment can have a long-lasting negative impact. Setting up auto-debit or payment reminders ensures that you never miss a due date.

It is also important to avoid frequent credit applications. Applying for multiple cards within a short period results in multiple hard inquiries, which can temporarily lower your score. Instead, users should focus on maintaining existing accounts effectively.

Lastly, keeping older credit cards active is beneficial. A longer credit history demonstrates stability and improves your overall credit profile. Even if you do not use an old card frequently, occasional transactions can help keep it active.

Internal Linking

To build a complete understanding of credit card usage, you should also explore related guides on CardMela. For example, learning advanced reward strategies through “How to Maximize Credit Card Rewards” can help you earn benefits while improving your credit score.

If your goal is long-term financial growth, the guide on “Financial Independence Using Credit Cards” explains how disciplined credit usage can support wealth building. Additionally, for users managing multiple cards, “How to Combine Multiple Credit Cards for Maximum Cashback” provides powerful strategies to optimize spending and utilization.These internal links create a strong content ecosystem that improves both SEO performance and user experience.

- How to Maximize Credit Card Rewards

- Financial Independence Using Credit Cards

- Best Cashback Credit Cards

External Linking

Understanding credit score guidelines from trusted sources is essential for making informed decisions. Organizations like the Reserve Bank of India provide regulations and financial awareness updates that help users stay protected.

Credit bureaus such as TransUnion CIBIL offer insights into how credit scores are calculated and what factors influence them. Referring to these sources ensures that your financial strategy is aligned with official standards.For regular transactions that help build credit history, platforms like Amazon and Flipkart can be used effectively with credit cards to maintain consistent activity.

Conclusion

Building a strong credit score is one of the most valuable financial achievements you can work toward, and credit cards provide a simple yet powerful way to achieve it. Every swipe you make is an opportunity to demonstrate financial discipline and strengthen your credit profile.

The journey to a high credit score does not require complex strategies or high income. It requires consistency, awareness, and responsible usage. By maintaining low utilization, making timely payments, and using the right credit cards, you can steadily improve your score and unlock better financial opportunities.

In the long run, a strong credit score reduces borrowing costs, increases financial flexibility, and opens doors to premium financial products. It is not just a number—it is a reflection of your financial reliability.

FAQs

Q1. How long does it take to build a credit score?

Usually 3–6 months of consistent usage.

Q2. What is the ideal utilization ratio?

Below 30%.

Q3. Can missed payments be fixed?

Yes, but it takes time.

Q4. Are secured cards useful?

Yes, especially for beginners.

Author Bio

A platform dedicated to helping users compare credit cards and make smarter financial decisions. He specializes in banking trends, AI in finance, and cashback strategies, providing practical insights to maximize savings and optimize

Whether you’re looking for cashback, travel rewards, fuel savings, or lifetime free cards — CardMela helps you compare, analyze, and choose the credit card that fits your lifestyle perfectly. We partner with leading partners to bring you exclusive offers and detailed insights, so you can make smart financial decisions with confidence.

© 2025 CardMela.com. All rights reserved.