Shocking: 83% of Indian Women Skip Job Applications Over Caregiving Burden

Table of Contents

Shocking: 83% of Indian Women Skip Job Applications Over Caregiving Burden

Introduction

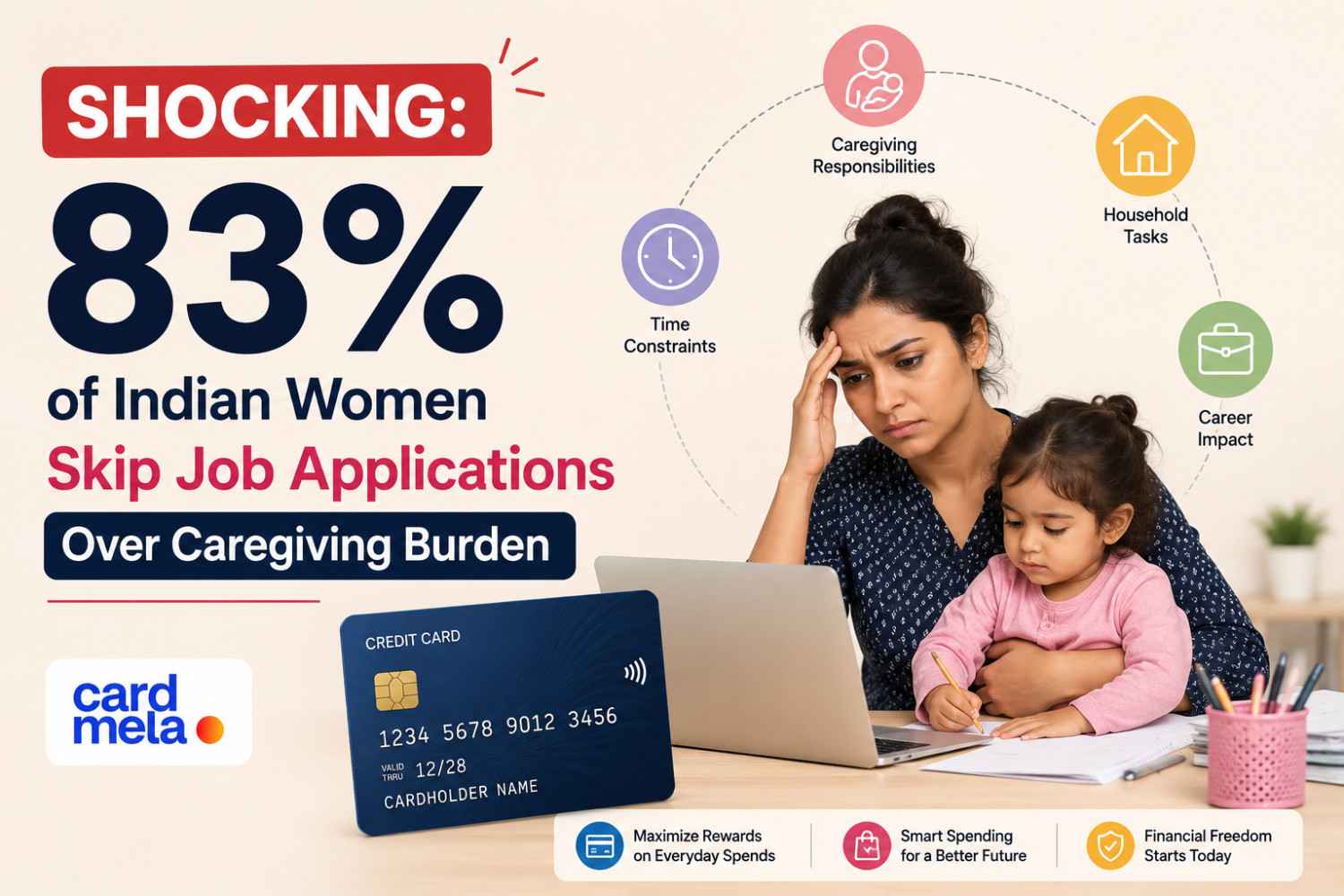

India’s workforce participation challenge among women has become one of the most important social and economic discussions in 2026. Recent reports and employment studies reveal that nearly 83% of Indian women avoid or skip job applications because of caregiving responsibilities, household pressure, childcare duties, elder care obligations, and limited workplace flexibility.

This growing issue is affecting not only career opportunities for women but also India’s long-term economic growth, digital workforce expansion, and financial independence ecosystem.

Across urban and semi-urban India, millions of educated women pause careers or reject job opportunities because balancing professional life and caregiving becomes financially, emotionally, and socially difficult.

Organizations such as the Reserve Bank of India and digital banking ecosystems are increasingly promoting financial inclusion initiatives aimed at empowering women financially through credit access, digital banking, savings awareness, and entrepreneurship opportunities.

At the same time, fintech platforms and banks are designing products specifically for women consumers including cashback cards, budgeting tools, savings-focused financial products, and flexible digital payment systems.

The conversation today is no longer only about employment. It is increasingly about financial independence, work-life flexibility, digital opportunities, remote work growth, and long-term wealth creation for women in India.

Understanding the financial impact of caregiving burden is essential because it directly affects household income, career progression, retirement planning, and overall economic participation.

Why Many Indian Women Skip Job Applications

Several interconnected reasons contribute to lower job participation among women in India:

- Childcare responsibilities

- Elder care obligations

- Household workload imbalance

- Lack of workplace flexibility

- Long commuting hours

- Safety concerns

- Career breaks after marriage or motherhood

- Limited support systems

- Financial dependency patterns

In many households, women continue managing unpaid domestic labor alongside emotional caregiving responsibilities, making traditional full-time employment difficult.

This issue affects women across education levels, income groups, and cities.

Financial Impact of Career Gaps on Women

Career interruptions often create long-term financial consequences including:

- Reduced savings growth

- Lower retirement planning

- Smaller investment portfolios

- Reduced credit eligibility

- Slower salary progression

- Financial dependency risks

Women taking career breaks may also face difficulty rebuilding professional confidence and re-entering competitive industries later.

This makes financial literacy and smart money management extremely important for women balancing caregiving and career responsibilities.

Benefits of Financial Independence for Women

Financial independence improves decision-making power, long-term security, confidence, and lifestyle flexibility.

Women with independent income sources often manage emergency situations more effectively and contribute strongly toward family wealth creation.

Financial awareness also helps women understand investments, taxation, insurance planning, digital banking systems, and credit score management.

Modern digital financial systems are making independent money management easier through mobile banking apps, UPI systems, online investments, and AI-based budgeting tools.

For many women, even part-time income or freelance work creates significant improvements in long-term financial stability.

Table: Major Challenges Faced by Working Women in India

| Challenge | Impact |

|---|---|

| Childcare responsibilities | Career interruptions |

| Elder care burden | Reduced work flexibility |

| Long commute times | Lower job participation |

| Workplace rigidity | High stress levels |

| Financial dependency | Lower savings growth |

Table: Financial Benefits of Career Participation

| Benefit | Long-Term Advantage |

|---|---|

| Independent income | Better financial security |

| Investment growth | Wealth creation |

| Credit score building | Easier loan approval |

| Retirement planning | Long-term stability |

Best Credit Cards for Working Women & Smart Financial Management

SBI SimplySAVE Credit Card

SBI SimplySAVE is suitable for women managing household spending, grocery shopping, and recurring family expenses efficiently.

HDFC Millennia Credit Card

HDFC Millennia works well for digitally active users seeking online shopping rewards, app-based spending benefits, and cashback opportunities.

Axis Bank ACE Credit Card

Axis ACE is highly useful for utility bill payments, online transactions, and cashback-focused financial management.

IDFC FIRST Select Credit Card

IDFC FIRST Select combines flexible rewards with lifestyle benefits suitable for working professionals and digitally active users.

Tata Neu Infinity HDFC Credit Card

Tata Neu Infinity helps users maximize rewards across shopping, groceries, travel, and UPI-linked transactions.

AU Bank LIT Credit Card

AU LIT offers customizable benefits, making it attractive for modern consumers seeking flexibility and app-based controls.

Table: Best Credit Cards by Lifestyle Need

| Lifestyle Need | Recommended Card |

|---|---|

| Household spending | SBI SimplySAVE |

| Online shopping | HDFC Millennia |

| Utility bill cashback | Axis ACE |

| Premium lifestyle | IDFC FIRST Select |

| UPI rewards | Tata Neu Infinity |

Explanation

The caregiving burden affecting Indian women reflects deeper structural and social challenges.

Traditionally, unpaid domestic responsibilities have been viewed primarily as women’s responsibilities. However, rising education levels, digital employment opportunities, and changing economic realities are gradually shifting this mindset.

Remote work, freelance platforms, digital entrepreneurship, content creation, online tutoring, and app-based work opportunities are helping more women participate economically while balancing family responsibilities.

Financial technology is also improving accessibility because women can now manage investments, savings, insurance, and banking directly through smartphones without visiting physical branches frequently.

Experts believe India’s economic growth potential can increase substantially if female workforce participation improves significantly over the next decade.

Uses

Financial literacy and smart banking tools help women in several ways:

- Managing household budgets

- Building emergency savings

- Starting investments

- Tracking expenses digitally

- Improving credit scores

- Managing family expenses efficiently

- Building independent income systems

- Supporting entrepreneurship

Credit cards with cashback and budgeting benefits additionally help users reduce recurring household costs while improving financial planning efficiency.

Women entrepreneurs and freelancers also use digital banking systems to separate personal and professional financial management more effectively.

Tips

Women managing caregiving responsibilities should prioritize financial independence even if income starts small.

Building emergency funds, learning digital banking systems, understanding investments, and maintaining healthy credit scores are important long-term financial habits.

Remote work opportunities, freelance platforms, and online skill development programs can provide flexible earning options without traditional office constraints.

Consumers should also avoid emotional spending and maintain clear monthly budgeting systems.

Using cashback-focused credit cards strategically for recurring expenses can help reduce household financial pressure over time.

Most importantly, women should actively participate in financial decision-making within households instead of depending entirely on others for money management.

Table: Smart Financial Habits for Women

| Habit | Financial Benefit |

|---|---|

| Emergency fund creation | Financial safety |

| Budget tracking | Better savings |

| Investment planning | Long-term wealth |

| Credit score management | Easier financial access |

Table: Common Financial Mistakes to Avoid

| Mistake | Risk |

|---|---|

| Ignoring savings | Financial instability |

| No emergency fund | Crisis pressure |

| Overspending online | Budget imbalance |

| Delaying investments | Lower wealth growth |

Digital Opportunities for Women in India

India’s digital economy is opening new career opportunities for women through:

- Freelancing platforms

- Remote jobs

- Content creation

- Digital marketing

- Online tutoring

- Ecommerce businesses

- Social media management

- AI-assisted work systems

Apps like LinkedIn and Upwork are helping skilled professionals access flexible work opportunities globally.

Experts believe hybrid work models and digital employment systems may significantly improve women’s workforce participation over the next few years.

Table: Future Workforce Trends for Women

| Trend | Impact |

|---|---|

| Remote work growth | Better flexibility |

| AI-based work tools | Higher productivity |

| Digital freelancing | Income opportunities |

| Flexible schedules | Better work-life balance |

Internal Linking

- Best Credit Cards for Household Expenses

- Best Cashback Credit Cards in India

- Best Credit Cards for Utility Bill Payments

- Best Credit Cards for Grocery Shopping

External Linking

Conclusion

The growing caregiving burden on Indian women highlights one of the most important workforce and financial challenges facing the country today. Career interruptions and reduced workforce participation not only affect women individually but also impact India’s broader economic potential.

However, digital banking systems, flexible work opportunities, fintech innovation, and growing financial awareness are gradually creating new pathways toward financial independence and career flexibility.

Women today have greater access than ever before to digital payments, investments, remote work ecosystems, and smart financial tools.

The future of financial empowerment in India will depend heavily on improving flexibility, encouraging financial literacy, supporting caregiving balance, and expanding inclusive economic opportunities for women across all income groups.

FAQs (Frequently Asked Questions )

Why are so many Indian women avoiding job applications because of caregiving responsibilities?

A large number of Indian women continue carrying the majority of household responsibilities including childcare, elder care, cooking, emotional support, and home management. These responsibilities often make traditional office jobs difficult to manage, especially when workplaces lack flexibility, remote work options, or supportive policies. Many women also pause careers after marriage or motherhood because balancing both professional and personal responsibilities becomes financially and emotionally exhausting.

How does caregiving burden affect women’s financial independence?

When women leave jobs or avoid employment opportunities, their long-term financial growth gets affected significantly. Career breaks reduce savings accumulation, retirement planning, investment opportunities, salary growth, and wealth creation potential. Financial dependency can also limit decision-making power and create future financial insecurity during emergencies or unexpected life situations.

Can remote work improve women’s workforce participation in India?

Yes. Remote work and hybrid job models are creating new opportunities for women who cannot manage long commuting hours or rigid office schedules. Work-from-home systems allow women to balance caregiving duties while continuing professional careers. Industries like digital marketing, content writing, customer support, online teaching, software services, and social media management are increasingly offering flexible work options.

Why is financial literacy especially important for women today?

Financial literacy helps women understand budgeting, savings, investments, taxation, digital banking, insurance, and credit management. Women who actively manage finances are usually better prepared for emergencies and long-term financial planning. Financial awareness also improves confidence and helps women participate equally in family financial decisions rather than depending entirely on others.

How can women start building financial independence with small income?

Women can begin financial planning by creating monthly budgets, opening savings accounts, starting SIP investments, building emergency funds, and tracking expenses digitally. Even small monthly investments made consistently can grow significantly over time through compounding. Freelancing, online businesses, tutoring, and digital content creation also provide additional income opportunities without requiring large investments.

Which credit cards are useful for women managing household expenses?

Cashback and rewards-focused credit cards are often useful for women handling grocery shopping, utility bills, digital payments, and family expenses. Cards such as SBI SimplySAVE, HDFC Millennia, Axis ACE, and Tata Neu Infinity provide rewards on recurring household spending categories. Responsible usage can help reduce monthly expenses while improving credit scores and digital payment convenience.

Author Bio

CardMela, a growing platform dedicated to helping Indian consumers make smarter financial decisions. Through CardMela, he focuses on credit cards, personal finance awareness, digital banking, budgeting strategies, and modern fintech trends designed specifically for Indian users.

Whether you’re looking for cashback, travel rewards, fuel savings, or lifetime free cards — CardMela helps you compare, analyze, and choose the credit card that fits your lifestyle perfectly. We partner with leading partners to bring you exclusive offers and detailed insights, so you can make smart financial decisions with confidence.

© 2025 CardMela.com. All rights reserved.